Do you wish you had cash to buy more rental properties? Are you facing a significant expense and you don’t have the funds? Maybe you are ready to retire and want to cash out your investments but still hang on to your rentals for future generations?

A cash out refi might be the answer for you. It was for me.

I have wanted to refinance the Adjustable Rate Mortgage on one of my rentals but never really felt the pressure in this low interest rate environment. That was until recently when rates started rising.

Faced with rising rates and looking for more cash to invest I decided to do a cash out refi.

I was able to lock in a good rate while extracting over $66k in equity. I can now put that cash to work in another rental, a flip, or invest in mortgage notes.

In this article I will:

- Explain what a cash out refi is

- Show you the 7 steps of the cash out refi process on a rental property

- Compare a cash out refi vs. HELOC and Home Equity loans

- Walk you through the numbers for my recent cash out refi

What Is Cash Out Refinancing?

Cash out refinancing (AKA a cash out refi), is simply a way to borrow against the equity in your rental property. You are borrowing more than you need to put some extra cash in your pocket.

It’s like when you use your credit card at the grocery store and the machine asks if you would also like cash back. Borrowing cash from your credit card is probably not a good financial move, but a cash out refi can be.

Here’s a simplified example:

- Rental Property Value = $150,000

- Current Debt = $70,000

- Current Equity = $80,000

In the above example, you have $80,000 of equity sitting in the rental property not doing anything productive. A cash out refi allows you to tap into that equity and start putting it to work for you.

Why Consider A Cash Out Refi?

There are several reasons why you might want to tap into the equity sitting idle in your rental properties.

Here are just a few:

- Buy more rental properties and expand your rental business (AKA the BRRRR method of investing

- Invest in other asset classes such as mortgage notes or crowd funded real estate investments

- Pay for unexpected capital repairs

- Retirement

- Consolidate and pay off higher debts

I’m sure you can come up with any number of reasons why you would want to get more cash in your pocket. The cash out refi is just a way to access that cash for whatever reason.

What Are The Advantages Of A Cash Out Refi?

There are several advantages of doing a cash out refi. Here are some of them:

Cheap Cash

When you do a cash out refinance on your rental property you paying off the old loan and creating a new loan. The new loan may be at a higher or lower rate but it will likely be a fixed mortgage. Fixed mortgages are cheaper than other ways of accessing your home equity.

Home Equity loan rates as of March 2019

Mortgage rates as of March 2019

You can see from the above rates that there is typically a 200 to 250 basis point spread in the rate you will pay depending on how you access your equity. That difference can easily add hundreds to your monthly interest expense.

Tax Deductible

Interest expense from a cash out refi loan on your rental property is tax deductible. Just like the original loan it is replacing, the interest expense can be used to offset your rental income.

This is also true for some of the closing costs you will pay to do a cash out refinancing.

Long Payback Period

Loan terms vary widely but the typical cash out refi is for 30 years. You may want to consider a 15 year mortgage if you’ve held the property for a while and want to be free and clear sooner rather than later.

Typical Home Equity loans are much shorter – Usually 5 to 15 years.

HELOCs allow you to draw from the line of credit for 10 years but then you have to begin repaying the loan over the next 15 to 20 years.

Disadvantages Of A Cash Out Refi

Wow! A Cash out refi sounds awesome! Where can I get one?

Hold on. You need to understand the implications of a cash out refi before you call your mortgage broker.

Extended Loan Period

A cash out refinancing will increase the amount of time you are in debt. You are trading your current mortgage, which has a remaining life of less than 30 years for a new 30 year loan. You can avoid this by opting for a shorter 15 or 20 year fixed mortgage but this will severely cut into your cash flows.

More Total Interest

A longer loan period means you will paying more in total interest over the life of the property. Even if you are able to secure a lower fixed rate on the cash out refi, you probably will still be paying more in the long run due to the extended years you will be paying interest.

Lower Cash Flow

A cash out refi loan will usually reduce your net monthly cash flows. Your new mortgage payment will be higher because you are borrowing more money than before.

Check out the example in my case study below to see how this works.

Higher Risk of Foreclosure

Lower net monthly cash flows increase your risk of foreclosure. The less cushion you have in your monthly cash flow, the more likely it is that a major expense could bankrupt your rental business.

Closing Costs

Cash out refis are not free. You can expect to pay anywhere between 2% to 5% of the loan amount according to NerdWallet. Since you are looking to maximize your cash in hand at the closing table, most investors roll these costs into the cash out refi loan itself.

Typical closing costs include Application fee, Origination fee, Appraisal, Broker fee, Recording fees, Points, Prepaid Interest and Property Taxes.

Cash Out Refi Vs. Home Equity Loans

Here is a quick comparison of Cash Out Refinancing vs. A Home Equity Loan to help you decide which form of financing is best for you.

| Cash Out Refi | Home Equity Loan | Home Equity Line Of Credit | |

|---|---|---|---|

| Interest Rate | • Fixed rate • +0.5% for investment property | • Fixed rate • +1.5% vs. Cash Out | • Variable rate • +2.0% vs. Cash Out |

| Term | • Up to 30 Years | • Up to 15 Years | • 5-10 Year Draw (Interest Only) • 10-20 Repayment (P&I) |

| Loan To Value | • Up to 80% • Best rate at 60% | • Up to 85% | • Up to 85% |

| Debt To Income | • 43% | • 43% | • Up to 50% |

| Disbursement | • Lump Sum | • Lump Sum | • As Needed |

| Closing Costs | • 2% - 5% of Loan | • 2% - 5% of Loan | • Origination Fee (up to $1,000) |

| Annual Fees | • None | • None | • $50 - $250 |

| Process | • Similar to home purchase (45-90 days) | • Similar to home purchase (45-90 days) | • Streamlined (30 days) |

Interest Rate

A fixed mortgage on an investment property will cost you .25% to .50% above a normal owner-occupied loan.

A Home Equity Loan will charge you another 1.50% above the Cash Out Refi rate on an investment property.

A Home Equity Line Of Credit will cost another 2.00% above the Cash Out Refi rate on an investment property.

Term

A fixed mortgage can typically run 15 to 30 years with anything in between. The longest Home Equity Loan will only be 15 years.

A Home Equity Line Of Credit is like a Credit Card but it is different in one big way. Unlike a credit card, which can carry a balance indefinitely, A HELOC must be repaid. You can borrow against the credit line for up to 10 years but then you need to start repaying the principal after that. Principal and Interest (P&I) payments can be extended for up to 20 years.

Loan To Value (LTV) Ratio

Fixed mortgages on an investment property can be taken for up to 80% of the value of the property. Some fixed mortgages will go up to 90% but these are rare. The rate you get will be significantly higher the higher the LTV ratio. I found the best break to be at around 60% LTV. Below that there are no more rate savings.

Both Home Equity Loans and HELOCs will let you borrow up to 85% of the value of the property. This includes the debt on the first mortgage as well.

Debt To Income (DTI) Ratio

Fixed mortgages and Home Equity Loans are similar in that they are each capped at 43% DTI. This means the total of your monthly debt payments cannot exceed 43% of your monthly income.

Some HELOCs can go as 50% DTI but this rare.

Disbursement Method

Fixed mortgages and Home Equity Loans are taken in lump sums at closing while HELOCs can be withdrawn as needed over the draw period (5-10 years).

Closing Costs

Fixed mortgages and Home Equity Loans have the highest closing costs at around 2-5% of the loan value. These are just like taking out a mortgage for the first time.

HELOCs have much lower closing costs but can vary widely. Shop around.

Annual Fees

Watch out for HELOC annual fees. They can hit you with a number of annual fees that can add up quickly.

Closing Process

Fixed mortgages and Home Equity Loans will take much longer than a HELOC because of the amount of paperwork and underwriting involved. Your lender will tell you about 30 days but be prepared for a longer process.

My fixed mortgage took over 60 days to close due to issues I mention below.

Other Considerations

- You will need more equity in your investment property due to the lower LTV if you plan to use a fixed mortgage

- Home Equity Loans and HELOCs can be difficult to get on an investment property. Your best bet is to check the local credit unions and regional banks first.

- HELOCs can be called or the terms can be changed at any time

- You may have to repay any lender-paid closing costs if you end a Home Equity Loan and HELOC before the contracted term

- The TCJA changed the tax deduction rules for second loans like Home Equity Loans and HELOCs. The interest may not be tax deductible anymore so be sure to check with a tax professional well versed in real estate and the new tax laws.

How Does Cash Out Refinancing Work?

A cash out refi works just like a getting a new mortgage because that’s exactly what it is. The process can easily take up to 60 days or longer and involves several steps.

Here are the steps you need to take when doing a cash out refi:

Step 1. Estimate Your Property Value

The first step when tapping into your home equity is to make sure you have a good estimate of how much your rental property is worth so you can determine how much equity is available. You don’t want to start the process and incur appraisal costs if you aren’t confident there is enough equity available.

To do this, you first need to estimate your property’s value.

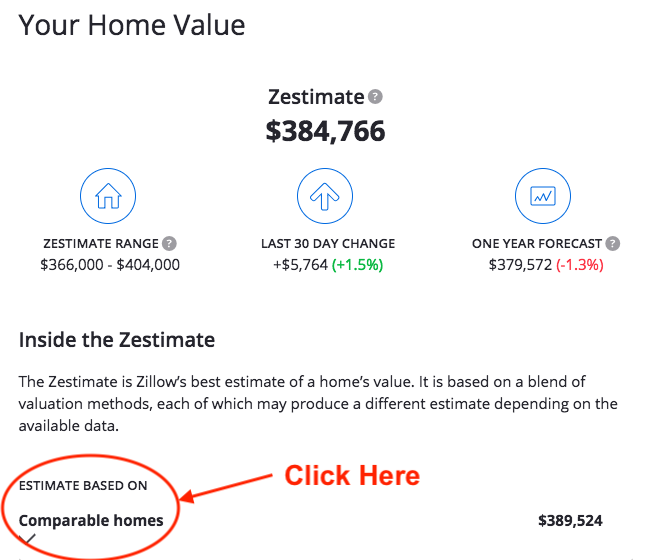

How To Estimate Value With Zillow

I like to start with the Zillow Comps.

- Log in to Zillow (create an account and claim your property if you haven’t already)

- Type in your address

- Scroll down to the Home Value and Zestimate section

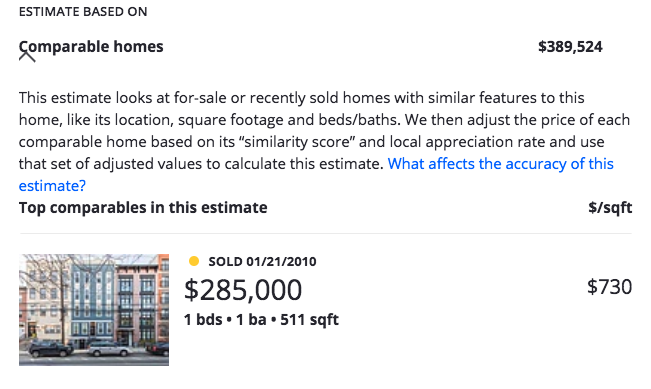

- Click on the Comps drop down to see the details of the properties they used to value your property. See example below.

A lot of experts will tell you to ignore the Zestimate because it has little correlation to the actual value of your property. Especially when it comes to rentals. However, if you are in a market with a lot of activity, as my rental is, then I think the Zestimate is in the ballpark.

How To Estimate Value With Realtors

You can also use your local realtors. Google “what’s my home worth?” You will get a number of ads for realtors willing to provide you a quick comp.

Here is an example of a realtor offering a free comp analysis I found via Google:

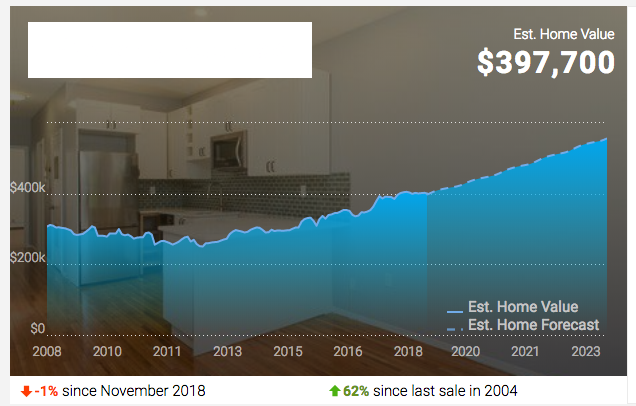

Realtor.com also provides a free snapshot estimate. Here is the one for my property that I refinanced.

As you can see, it’s pretty easy to get a rough idea of what your property is currently worth. Don’t skip this step because you think you know what it is worth. Confirm the value before moving forward.

Step 2. Estimate Your Available Equity

Now that you know roughly what your rental property is worth, you calculate your available equity.

- Multiply the estimated property value by your anticipated LTV (most will be 80%)

- Subtract your current mortgage and other debt against the property

- What’s left is your available cash BEFORE fees and closing costs

Estimate 2-5% for loan fees if you want a more accurate estimate of how much cash you can get from your rental.

Cash Out Refi Calculation Example:

| Property Value | $275,000 |

| 80% LTV | 80% |

| Max Loan Value | $220,000 |

| Subtract Current Debt | -$125,000 |

| Available Cash | $95,000 |

| Subtract 4% Closing Costs | -$3,800 |

| Net Cash Out Refi | $91,200 |

Step 3. Find A Lender Or Mortgage Broker

Do yourself a favor and shop around for the best lender when doing a cash out refinancing. The fees and rates will vary a lot so you need to do some comparisons.

The best way to compare different loans is to make use of the Good Faith Estimate form. All lenders are required by law to give you an estimate of all the costs of the loan.

Here’s an example from HUD:

PRO TIP – Don’t forget to negotiate! Some costs such as lender’s fees, interest rates, points, title insurance, and escrow fees are negotiable. It never hurts to ask. You know you’ve found the best deal when you can’t negotiate any further.

Work With A Trusted Broker

The advantage of working with a mortgage broker is that they will do the comparison shopping for you. They also have access to wholesale rates. They will mark up the wholesale rate a bit and charge you some fees on top, but the net affect is often a better deal than you can get on your own.

Keep Them Honest

I like to work with a broker of mine that I have used for years. But I also keep him honest by spot checking his rates against other local and big bank lenders. He has always come up with the better deal but it pays to check any way.

I was getting close to closing on my cash out refi when I decided to check on rates one more time. My broker said rates were about the where they had been. I checked with another local bank just to be sure. They said their rates had just dropped. I went back to my broker and asked for the lower rate. He gave it to me.

Those two emails saved me over $5,000!

Use An Online Comparison Tool

Bankrate.com has a pretty good loan comparison tool. It’s not pretty but it has inputs for more closing costs than most similar tools. It comes in very handy when evaluating multiple cash out refinancing loan offers.

The number are important but there are other factors to consider when choosing a lender. Money.com has a great article that recommends the best lenders on several attributes such as customer service and transparency. Check it out before you choose a lender.

Step 4. Gather Paperwork. Lots Of Paperwork.

This is the most painful part of the cash out refi process. The digital revolution seems to have left the real estate industry behind.

Here is a list of the common documentation you will need as soon as you engage a lender or broker:

- 1 or 2 years of tax returns

- Two months of bank, 401(k), IRA statements. etc.

- Copy of your current lease if your home is a rental

- Proof of income (usually 1-2 months of W-2s)

- Copy of all mortgage statements for all properties owned

- Proof of Homeowner’s / Landlord insurance for all properties owned

- Signed letter explaining why you want the cash

- HOA questionnaire

- Photocopy of Drivers licenses

This list is not meant to be comprehensive. Your lender or broker may require more documentation.

Step 5. Follow Up On Any Requests

You can expect a number of questions to come up during the mortgage underwriting process. That’s because most loans that go to underwriting are “approved with conditions.” They need more information to make sure everything is ok before they clear you to close.

Typical requests can include things such as:

- More information on former addresses

- Clarify specific financial transactions

- Explain gaps in employment

As ridiculous as some of these requests may seem, they are necessary to get your cash. Don’t take them personally. Just give them the answers ASAP to keep the process moving.

I got hung up on not having adequate flood and home insurance. The home insurance was no problem. It only cost me an extra $30. But the flood insurance was a hassle because I had to go through the HOA.

Just one more reason why I don’t like renting out condos.

Step 6. The Appraisal

The appraisal is where you will find out how much you will be able to borrow for real. Once you provide most of the paperwork and it looks like the loan will go through, the lender will authorize the appraisal.

The property appraisal process is a whole other topic but here is a great article explaining them.

Make sure you have a good estimate of the value and that the loan will likely go through because you will be on the hook for the appraisal costs if you back out or if it comes in too low afterwards.

Step 7. Collect Your Cash

Now you’re ready for the best part – collecting your cash at closing!

You just need to bring proof of identification and be ready to sign way too many forms (why so much paper?!?)

PRO TIP. Make note of when your first payment is due. It will usually be up to 60 days after the close. You skip the next month’s payment but you still owe the interest on it. Also be sure to ask when you can expect to receive your escrow funds back from the previous mortgage company. This can easily take 30 days or more. It has about 40 days since my close and I am still waiting.

My Cash Out Refi Case Study

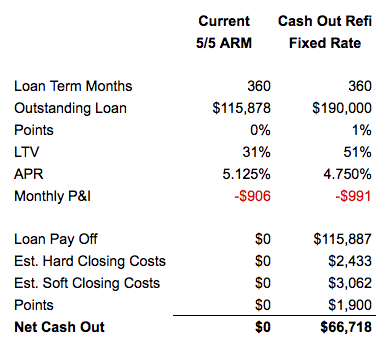

My cash out refi was a little different than the typical one. I needed to get rid of my variable rate loan that was creeping up and eating into my monthly cash flow.

It was a no brainer to take advantage of the situation and do a cash out refi to put some extra cash in my pocket in the process.

My Estimated Equity

| Estimated Property Value | $375,000 |

| Outstanding Loan | $115,887 |

I estimated my value at $375,000 to play it safe. It ended up being $390k according to the appraiser. Zillow and others were pretty close to this as well as I showed above.

Here’s how the numbers on my cash out refi shook out.

My goal was to take out as much cash as possible but still leave myself at little bit of cash flow every month. I already have a good CapEx Reserve for this property but I still wanted a little buffer to cover rising taxes, HOA or whatever.

I chose to hold the P&I to no more than $1,000 so that meant I could only take out $190k. It also meant I needed to buy down the rate with 1 point.

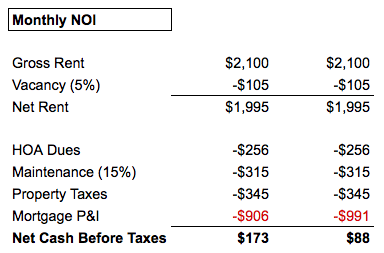

Before & After Monthly NOI

You can see from the above comparisons, I was able to take out $67k but it only cost me cost me $85 of monthly cash flow.

Previously I was clearing approximately $173 per month after all cash expenses including allocating for vacancies and maintenance.

After the cash out refi I was left with a buffer of only $88/month. It may not seem like much but remember that I am covering my mortgage and as well as all my other cash costs.

My Cash Out Refi allowed me to pull out about $67k of equity from my property that I can now put to better use.

Now I have enough cash in my pocket to invest in another rental or loan it out at 10-12%. Either way, I will end up with two assets instead of one.

That is how you make your money work for you and not the other way around!

Conclusion

A cash out refi can be a great way to leverage the equity in your rental properties. It’s main advantage over other types of equity loans is that it gives you relatively cheap access to cash. However, there are some drawbacks to a cash out refi so you need to do a thorough before and after analysis to see if one makes sense for you.

This article reviewed the 7 steps of a cash out refi on a rental property.

Start by estimating the value of your property and calculating how much equity you can tap into using the appropriate LTV ratio.

Next, find a mortgage broker and negotiate the best possible terms. Prepare your documents and be ready to follow up on any requests quickly to keep the process moving.

Finally, collect your cash and start putting your rental property equity to work for you!

Want More Landlord Tips?

Sign up today for the Accidental Rental monthly newsletter for access to more tips and tricks that can help you become a successful landlord!

Very informative! Thank You.

N

Mike Justice, Wallingford KY